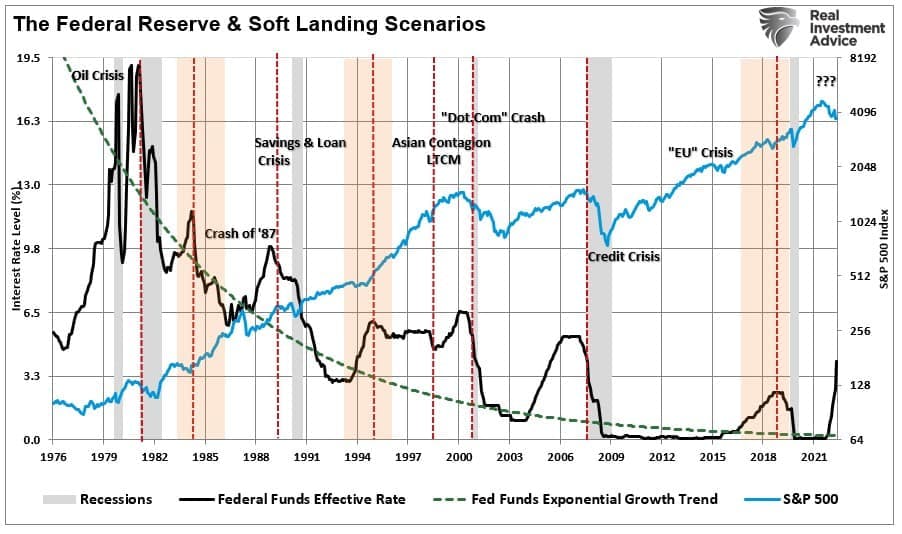

Fed being data dependent?

In CB jargon, data-dependent means the market is pleased to go ahead and price whatever you want. Monetary policy decisions must be made with an eye toward the future. It is well-known that monetary policy operates with long and variable lags. Accordingly, the monetary policymaker must incorporate forecasted future outcomes when making current monetary policy decisions. Although macroeconomic forecasts are changed in response to new data, the changes tend to depend on whether a particular piece of data was expected and how important it is relative to other pieces of data. Given that the contours of forecasts do not change very quickly, monetary policy strategy also does not change very quickly. However, both probably would change in response to an ongoing slew of worse-than-expected or better-than-expected data.

MARKETS IN A BRIEF

On Thursday we had a so-called “Golden cross” in the S&P500 market. This is a technical indicator for those who do not know when we see the 50-day average of the market cross above its 200-day moving average.

In past, the results of such a moving average cross have been very impressive:

The last time it happened was in July of 2020 when the S&P500 rose about 35% a year later!

Before that this happened in 2016 when the market rose about 30% a year later!

I also will question relying on the Golden cross to call a bull market when we are in historic inflation (compared to the last twenty years or so).

Inflation hedge?

Now speaking of an inflation hedge, yet again we saw a rally in Bitcoin which was fueled by a surge in growth rather than it being an inflation hedge - Bitcoin rallied almost to 24000 fueled by this rotation- this proves yet again Bitcoin is not an inflation hedge. It is a highly speculative instrument that relies on Dollar's demise to make gains - I think Bitcoin will eventually trade at $9000 even lower.

Consumer staples, especially some well-known brands, are often viewed as safe havens.

Is playing with the debt ceiling a safe play?

T-Bills: In 2023, let’s assume a current average yield of 4.5%, which would result in $180 billion in interest expense.

Basically, servicing T-bills will have gone from somewhere close to 0 in 2021 to close to $200 billion in 2023 (with 2022 somewhere in between). The Fed “only” owns $280 billion of T-bills (7% of the total). Given that the Fed funds at roughly that rate, it is kind of a “net” wash – the Fed gets 4.5% on T-Bills and pays about the same on excess reserves. This becomes “interesting” if any games are played in terms of how the T-bills held by the Fed count towards the debt ceiling (but the coupon market is where the bigger notional amounts are at play).

Questions:

1) Would the stock market tumble precipitously the first day that a Social Security payment is delayed?

2) Would the U.S. Treasury market, the world’s most important, function smoothly?

3) Would there be a run on money market funds that hold short-term U.S. Treasuries?

4) What actions would the Federal Reserve take to stabilize financial markets and the economy more broadly?

Regardless, even if the debt limit were raised quickly so that it only was binding for a few days, there could be lasting damage. At the very least, financial markets would likely anticipate such disruptions each time the debt limit nears in the future.

Worsening expectations regarding a possible default would make significant disruptions in financial markets increasingly probable. That could result in an increase in interest rates on newly-issued Treasuries. If financial markets started to pull back from U.S. Treasuries altogether, the Treasury could have a difficult time finding buyers when it sought to roll over maturing debt, perhaps putting pressure on the Federal Reserve to purchase additional Treasuries in the secondary market.

Such financial market disruptions would very likely be coupled with declines in the price of equities, a loss of consumer and business confidence, and a contraction in access to private credit markets.

Given that those disruptions would likely occur when the economy is growing slowly and perhaps contracting, the risk that the crisis would quickly trigger a deep recession is heightened. Moreover, tax revenues, the only resource the Treasury would have to pay interest on the debt, would be dampened, and the federal government would have to cut back on non-interest outlays with increasing severity.

AFFECT: Increase in 10-year Treasury yields, a decline in stock prices, a decline in the value of the dollar, a hit to household and business confidence.

Why did VIX lose its importance as a risk parameter?

You can stare at VIX all you want, but you are unlikely to get much useful information. Speculators, vol sellers, covered call sellers, and hedges have all moved their money from the more expensive options (included in the VIX options) to less expensive options. Some option purists will scream bloody murder that the daily option implied volatility is way more expensive than it is in the longer-dated options, but they are being too smart for their own good as this is about leveraged dollars, not trading implied versus realized volatility.

Buy at the wrong price, you'll pay dearly for it.