If Everyone Agrees, It May Not Happen.

“FeD cReDiBiLiTy”

Federal Reserve officials are on track to consider pausing interest-rate hikes following their March meeting if more evidence of cooling inflation rolls in.

So YES, inflation data is showing what we all knew would be an inevitable “mathematical” disinflation vs prior year comps - but that data is lagging the reacceleration in both US and global overall economic activity... and that is why folks are suddenly waking up to the risk that Fed may have fallen-behind again.

So I would expect a lot of 'data dependent' references from Powell and Fed speakers in the coming days, versus the prior THIRTEEN MENTIONS of “disinflation” like last Weds.

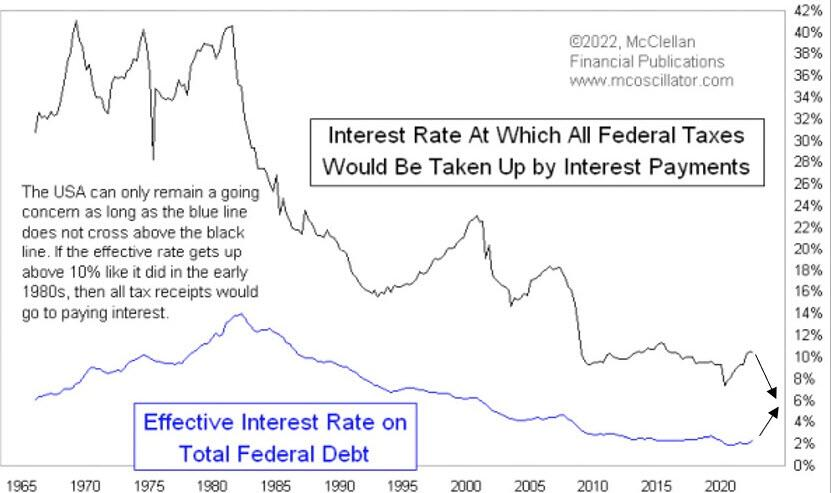

Ever-increasing debt is manageable if interest rates fall concurrently so the interest on that debt doesn’t change. And that’s what happened between 1980 and 2021. The Fed pushed down interest rates, which minimized interest costs, which lulled a shockingly gullible investment community and political class into the belief that this process could continue forever.

DEATH SPIRAL: which will require more borrowing, and so on, until it all comes crashing down.

Here’s another useful way of visualizing the problem. As debt rises, the interest rate required to keep debt service costs from eating all of a government’s tax receipts falls. In the US case, those two lines are in danger of crossing in the next few years. No society has ever survived that kind of fiscal crisis.

To the extent that the Fed knows anything, it knows this, and really, really wants to force that blue line down into negative territory if possible. But it also knows that doing so will send prices spiraling out of control – which is another way of saying the dollar will crash (not necessarily against the euro and the yen, which have similar problems, but against oil, lumber, eggs, milk, cars, and all the other things voters buy regularly). The result? Political and financial chaos.

Questions:

Ongoing or expected “disinflation"?

Hikes will be appropriate?

The risk of doing too little?

Another gamma squeeze?

PRICED OR NOT PRICED?

(POWELL) he doesn’t want to find out in six to 12 months that they were “close but didn’t get the job done.

Overtightening seemed less worrisome.

MARKETS:

Most of the S&P 500 options action WAS ahead of Fed Chair Powell’s noon remarks on Tuesday and has been put buying, with the majority of the volume is for strikes at 4100 and 4050.

This is a problem because if Powell is not hawkish enough, and stocks don't tumble (as a reminder, a potential hawkish segue by the Fed chair was generally priced into stocks today), then all those puts will quickly collapse in value, leading to a rapid liquidation which in turn will force the dealer community to cover their delta hedges and aggressively bid up markets (into the traditional illiquid tape)

"If comments by Powell tomorrow don’t lean hawkish, the asymmetric risk is clearly skewed to the upside with a squeeze for a risk rally for stocks and bonds accompanied by a dollar selloff."

“Resumption of Hiking” [ WE ARE IN THE UNKNOWN SEAS]

THE CYCLE: Economic Reacceleration = Reflation = Resumption of Fed Hikes, Post-Pause” scenario is suddenly the BASE-case

All Rights Reserved.

Any reproduction, copying, or distribution, in whole or in part, is prohibited without permission from the publisher. Information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal circumstances–we are not financial advisors and do not give personalized financial advice. The opinions expressed here are those of the publisher and are subject to change without notice. It may become outdated and there is no obligation to update any such information.

Investments should be made only after consulting with your financial advisor and only after reviewing the prospectus or financial statements of the company or companies in question. You shouldn’t make any decisions based solely on what you read here. Neither MarketSumm nor its employees and writers receive any compensation for securities or investments covered herein.